This week, Westpac Banking Corporation - the oldest bank in the country, and one of the big four - released its first half profits.

Buried within its presentation to investors, was a massive change to its lending standards for oil and gas producers and explorers.

During the first half, Westpac undertook what it called a "transition risk analysis" and developed a new assessment criterion it will follow when considering financing for the oil and gas sector.

It will not just affect whether oil and gas explorers and producers are able to secure finance, but also the petrochemical and refining industries.

Under the newly minted policy, oil and gas companies will need to show how their operations are aligned with the emissions reductions set out under the Paris Agreement.

"We will expect any new oil and gas exploration, production and refining customers, to whom we provide lending, to have publicly disclosed Paris-aligned business goals," Westpac said.

It will also require existing companies it lends to, including Woodside Petroleum and Santos, to develop Paris-aligned finance strategies, and have a path towards decarbonisation.

Westpac is now one of the first banks in the world to implement this rule.

According to its latest financials, the bank has already been decreasing its finance lending to Australian oil and gas companies.

In March last year it had an exposure of about $3.3 billion in the upstream oil and gas sector. This fell to $2.8 billion in September 2020. And it is currently worth about $2.3 billion.

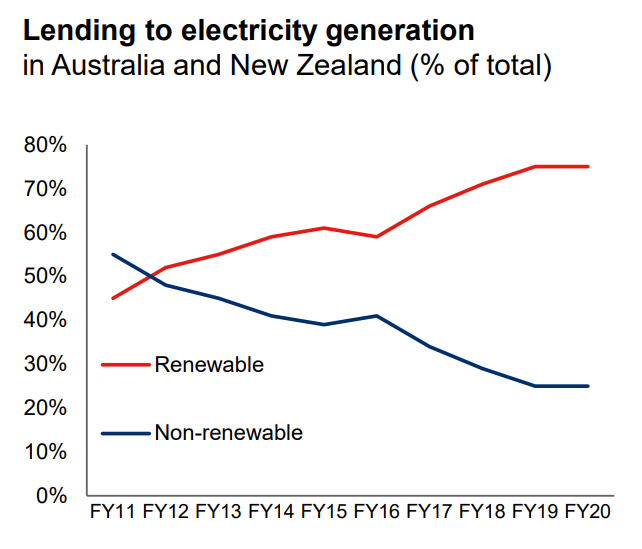

Downstream, in the electricity generation sector, Westpac exposure is worth $4.3 billion. Of this, 15.6% is for gas generation projects, or roughly $671 million. The majority, 74.6%, of finance in energy generation is actually for renewables, worth approximately $3.2 billion. Black coal generation exposure is just 6.4%, or $275 million.

Westpac shares were down 1.4% after jumping yesterday from $24.91 to $26.28 per share. This was partly due to the chief executive's announcement that he would look to cut $200 billion from operational costs - namely, closing local branches and staff.

In October ANZ announced similar policies, saying it would lobby major oil and gas companies to establish and strengthen their energy transition plans by 2021, and from that date would set targets to reduce the financed emissions of each sector between now and 2030.

The decision sparked outrage amongst National Party MPs who declared banks are "not a moral compass".

"Banks are not and should not try to become society's moral compass and arbiter - the Australian people decide that, by who they elect," agriculture and drought minister David Littleproud said.

"We can't let unelected profit-driven financiers from Pitt Street dictate to society how to produce food and fibre or how we run our economy."